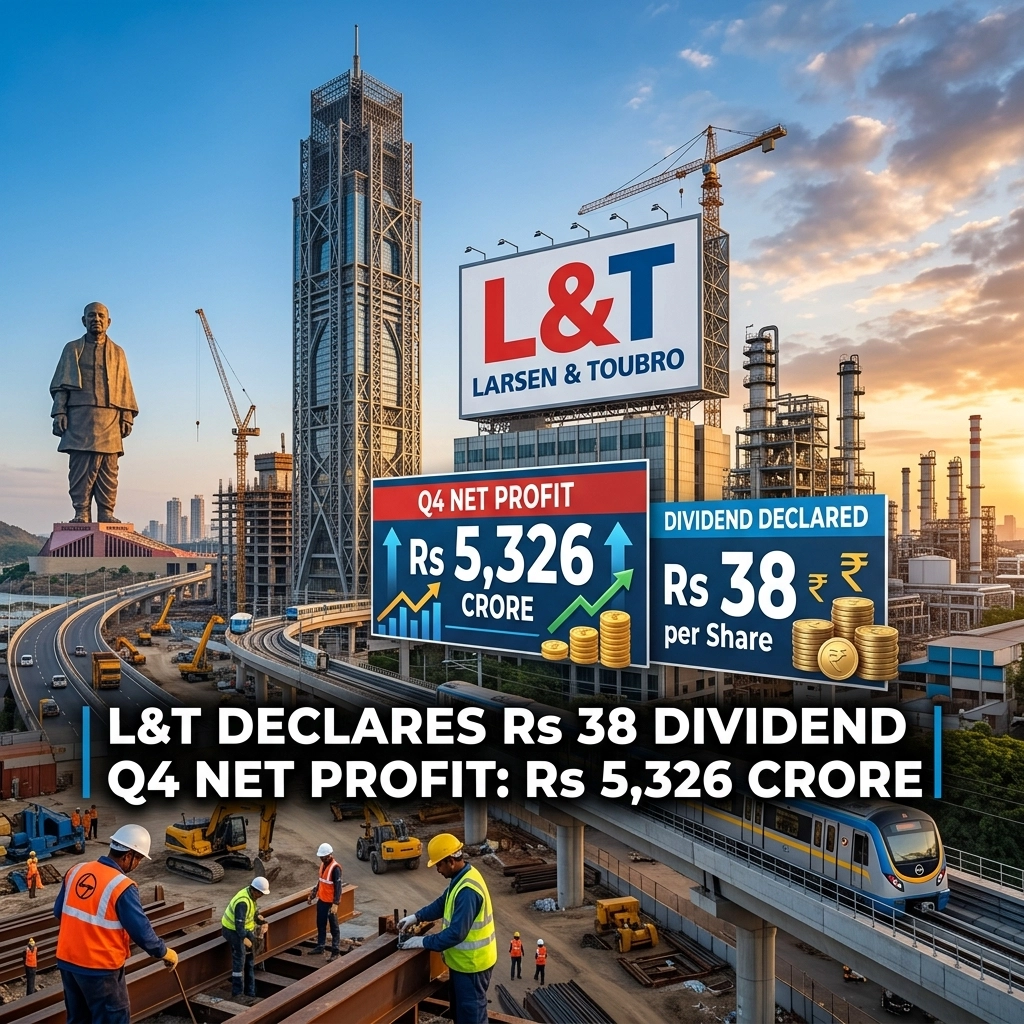

Larsen & Toubro (L&T), the quintessential bellwether of the Indian infrastructure and engineering landscape, has officially released its L&T Q4 Results for the fiscal year ending March 2026. In a complex macroeconomic environment characterized by fluctuating commodity prices and geopolitical shifts, the conglomerate reported a consolidated net profit of Rs 5,326 crore. While this figure represents a marginal 3% year-on-year (YoY) decline compared to the Rs 5,487 crore recorded in the corresponding quarter of the previous year, the company’s broader financial health remains robust, underscored by a record-breaking order book and a significant dividend declaration for its shareholders.

The Board of Directors has recommended a final dividend of Rs 38 per equity share, a move that signals management’s confidence in the firm’s long-term value proposition and cash flow stability. This announcement comes at a pivotal moment as the Indian stock market navigates through the volatility induced by a record-low Rupee and renewed international tensions.

Unpacking the Financial Metrics: Revenue and Profitability

Despite the slight contraction in the bottom line, L&T’s top-line performance remains on an upward trajectory. The company reported an 11% increase in consolidated revenue, reaching a scale that reflects the continued momentum in domestic infrastructure execution. The 3% dip in net profit is primarily attributed to heightened operational costs and the tail-end impact of inflationary pressures on legacy projects.

Key Financial Highlights:

- Net Profit: Rs 5,326 crore (Down 3% YoY)

- Revenue: 11% Growth YoY

- Dividend: Rs 38 per equity share

- Order Book: Reached a fresh record high

For investors and market analysts, the L&T Q4 Results serve as a critical indicator of the health of the Indian industrial sector. The ability to maintain a profit margin exceeding Rs 5,000 crore amidst global headwinds is a testament to the company’s diversified business model and its strategic focus on high-margin international and domestic contracts.

The Rs 38 Dividend: A Catalyst for Investor Confidence

The declaration of an Rs 38 per share dividend is the standout feature of this quarter’s announcement. For a company of L&T’s scale, such a payout is not merely a distribution of surplus but a strategic signal to the capital markets. In an era where many tech-heavy firms are struggling with liquidity, L&T’s "old economy" resilience provides a sense of security to institutional and retail investors alike.

This dividend payout reflects the company's commitment to returning capital to its stakeholders, even as it continues to invest heavily in futuristic segments like green hydrogen, data centers, and semiconductor design. As the Indian economy continues its rebound, large-cap entities like L&T are increasingly focused on maintaining high ESG (Environmental, Social, and Governance) standards while ensuring consistent shareholder returns.

Record Order Book: Ensuring Long-Term Revenue Visibility

One of the most optimistic data points in the L&T Q4 Results is the record-high order book. While specific figures fluctuate with monthly intake, the cumulative backlog has reached an unprecedented peak, providing multi-year revenue visibility. This "moat" protects the company against short-term cyclical downturns in any specific sub-sector.

The order book is increasingly diversified across several key verticals:

- Infrastructure: Driven by the Government of India’s continued push for high-speed rail, expressways, and urban transit systems.

- Energy: Significant gains in hydrocarbon projects and renewable energy transitions.

- Hi-Tech Manufacturing: Pivoting toward defense and aerospace components.

The execution of these orders is vital for the company's "exponential growth" strategy. However, the management has cautioned that rising consumer price indices and supply chain disruptions can impact the "legitimate purpose" of cost-efficiency. To mitigate this, L&T has been increasingly utilizing "data-driven insights" to optimize procurement and project timelines.

Segmental Performance and Operational Resilience

L&T's performance must be viewed through the lens of its various business segments. The Infrastructure segment continues to be the largest contributor to the revenue pie, benefiting from the "Modi wave" of capital expenditure as seen in the rise of Indian startups and industrial parks.

Infrastructure and Energy

The core engineering, procurement, and construction (EPC) business faced some margin contraction due to higher input costs. However, the international segment, particularly in the Middle East, has shown remarkable resilience. The company's "mission" to democratize high-end engineering solutions globally has seen it win massive orders in Saudi Arabia and the UAE.

IT and Technology Services

The services arm, including LTIMindtree and L&T Technology Services, continues to provide a stable cushion of high-margin revenue. As global enterprises shift toward AI-driven operations, L&T’s tech subsidiaries are well-positioned to capture the next wave of digital transformation. This is a sharp contrast to the layoffs seen in pure-play tech firms like Coinbase, as L&T's tech offerings are deeply integrated into physical engineering and manufacturing processes.

Macroeconomic Headwinds: The Rupee and Global Tensions

The L&T Q4 Results were announced against a backdrop of a record-low Indian Rupee, which plummeted as US-Iran tensions flared up once again. For a conglomerate with significant international debt and large-scale import requirements for raw materials, currency volatility is a persistent risk.

Furthermore, the maintenance shutdown of major refineries, including those of Reliance Industries, could have a ripple effect on the industrial output that L&T supports. Management remains optimistic, however, noting that the company's diversified geographic footprint acts as a natural hedge against localized economic shocks.

Strategic Outlook: 2026-27 and Beyond

Looking ahead, L&T is focusing on revitalizing its "value proposition" by integrating sustainable practices across its supply chain. The company’s foray into green energy and battery swapping is expected to become a major revenue driver by the end of the decade.

The board’s decision to maintain a high dividend payout despite a slight profit dip suggests a shift toward a more "investor-friendly" capital allocation framework. By balancing the need for massive R&D investments with the necessity of rewarding long-term shareholders, L&T is positioning itself as a stable anchor in a volatile market.

Market analysts from leading firms suggest that while the 3% profit dip is a "minor speed bump," the record order book is the "true catalyst for change." As long as the execution pace matches the order inflow, the company is likely to see a significant re-rating in the coming quarters.

Conclusion

The L&T Q4 Results for 2026 present a nuanced picture of a corporate giant that is successfully navigating a transition period. While the net profit of Rs 5,326 crore indicates a slight YoY retreat, the 11% revenue growth and the record-shattering order book tell a story of sustained industrial demand. The declaration of an Rs 38 per share dividend serves as a robust vote of confidence in the company's financial resilience and its ability to generate cash in challenging times.

For the Indian stock market, L&T remains a cornerstone of the industrial narrative. As the company continues to execute on its massive backlog and explores new frontiers in green technology and hi-tech manufacturing, it solidifies its role as an indispensable driver of India’s economic aspirations. Investors should look beyond the immediate profit fluctuation and focus on the structural strengths: diversified revenue streams, technological integration, and a shareholder-centric approach: that define Larsen & Toubro today.