TEMPE, AZ — Economic activity in the manufacturing sector grew in February, with the overall economy achieving a 21st consecutive month of growth, say the nation’s supply executives in the latest Manufacturing ISM Report On Business.

The report was issued today by Timothy R. Fiore, CPSM, C.P.M., Chair of the Institute for Supply Management (ISM) Manufacturing Business Survey Committee:

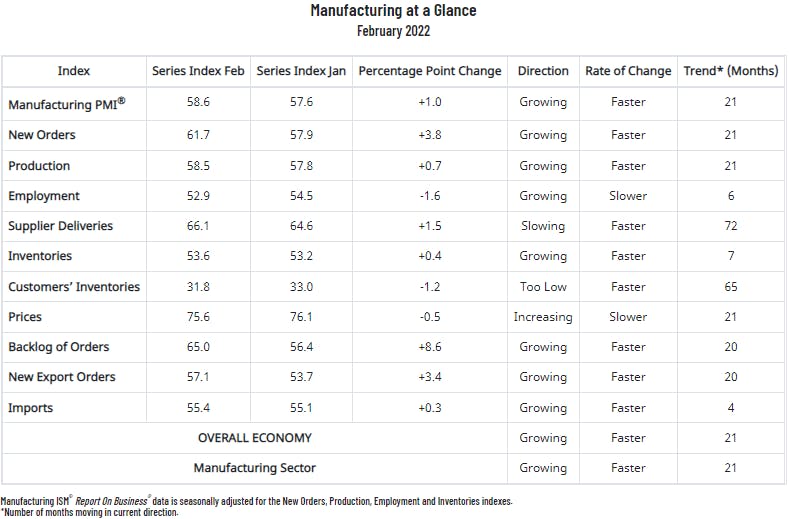

“The February Manufacturing PMI registered 58.6 percent, an increase of 1 percentage point from the January reading of 57.6 percent. This figure indicates expansion in the overall economy for the 21st month in a row after a contraction in April and May 2020. The New Orders Index registered 61.7 percent, up 3.8 percentage points compared to the January reading of 57.9 percent. The Production Index registered 58.5 percent, an increase of 0.7 percentage point compared to the January reading of 57.8 percent. The Prices Index registered 75.6 percent, down 0.5 percentage point compared to the January figure of 76.1 percent. The Backlog of Orders Index registered 65 percent, 8.6 percentage points higher than the January reading of 56.4 percent. The Employment Index registered 52.9 percent, 1.6 percentage points lower than the January reading of 54.5 percent. The Supplier Deliveries Index registered 66.1 percent, an increase of 1.5 percentage points compared to the January figure of 64.6 percent. The Inventories Index registered 53.6 percent, 0.4 percentage point higher than the January reading of 53.2 percent. The New Export Orders Index registered 57.1 percent, up 3.4 percentage points compared to the January reading of 53.7 percent. The Imports Index registered 55.4 percent, a 0.3-percentage point increase from the January reading of 55.1 percent.”

Fiore continues, “The U.S. manufacturing sector remains in a demand-driven, supply chain-constrained environment. The COVID-19 omicron variant remained an impact in February; however, there were signs of relief, with recovery expected in March. A higher-than-normal quits rate and early retirements continued. Panel sentiment remained strongly optimistic, with 12 positive growth comments for every cautious comment, up from January’s ratio of 7-to-1.

- Demand expanded, with the (1) New Orders Index increasing and remaining in strong growth territory, supported by stronger expansion of new export orders, (2) Customers’ Inventories Index remaining at a very low level and (3) Backlog of Orders Index increasing to historically high levels.

- Consumption (measured by the Production and Employment indexes) grew during the period, though at a slower rate, with a combined minus-0.9-percentage point change to the Manufacturing PMI calculation. The Employment Index expanded for a sixth straight month; panelists indicate their ability to hire continues to improve, but to a lesser degree than in January. Challenges with turnover (quits and retirements) and resulting backfilling continue to plague panelists’ efforts to adequately staff their organizations. Production expanded satisfactorily, despite staffing and supplier delivery headwinds.

- Inputs — expressed as supplier deliveries, inventories, and imports — continued to constrain production expansion. The Supplier Deliveries Index again slowed at a slightly faster rate, while the Inventories and Imports indexes increased, both at slightly faster rates. In February, the Prices Index increased for the 21st consecutive month, at a slightly slower rate.

“All of the six biggest manufacturing industries — Transportation Equipment; Machinery; Computer & Electronic Products; Food, Beverage & Tobacco Products; Chemical Products; and Petroleum & Coal Products, in that order — registered moderate-to-strong growth in February.

“Manufacturing performed well for the 21st straight month, with demand registering month-over-month growth and consumption softening slightly, though less than forecast. The impact of omicron declined in February as swiftly as it appeared in December, leaving March and April’s manufacturing environment favorable, especially with new orders and backlogs registering strong growth,” says Fiore.

The 16 manufacturing industries reporting growth in February — in the following order — are: Apparel, Leather & Allied Products; Textile Mills; Paper Products; Transportation Equipment; Machinery; Miscellaneous Manufacturing; Primary Metals; Electrical Equipment, Appliances & Components; Computer & Electronic Products; Furniture & Related Products; Plastics & Rubber Products; Fabricated Metal Products; Food, Beverage & Tobacco Products; Nonmetallic Mineral Products; Chemical Products; and Petroleum & Coal Products. The only industry reporting a decrease in February compared to January is Wood Products.

WHAT RESPONDENTS ARE SAYING

- “Electronic supply chain is still a mess.” [Computer & Electronic Products]

- “Strong sales growth as retail continues to return.” [Chemical Products]

- “Demand for transportation equipment remains strong. Supply of transportation services continues to be a major issue for the supply chain.” [Transportation Equipment]

- “Strong demand has continued beyond our traditional seasonality curves. Coupled with the continuing difficulties in procurement of ocean freight, operational planning and managing costs are our biggest challenges.” [Food, Beverage & Tobacco Products]

- “We have seen year-over-year revenue growth of about 10 percent due to markets coming back. However, in the automotive area, the microchip shortage is causing slowness in growth.” [Machinery]

- “Demand for steel products has increased to historic levels, driven by the automotive and energy industries.” [Fabricated Metal Products]

- “We are expecting a year of strong demand, higher prices and continued supply chain challenges.” [Textile Mills]

- “Demand continues to be strong, increasing our backlog. Production has been more consistent due to availability of parts, but we are not able to increase builds to cut into the backlog.” [Electrical Equipment, Appliances & Components]

- “Business conditions are good, demand remains strong, and we continue to be challenged to keep up with demand.” [Miscellaneous Manufacturing]

- “Business is still strong. Facing logistics and raw material supply chain issues with some products.” [Plastics & Rubber Products]